Investing wisely is key to building long-term wealth and securing your financial future. Many people seek professional help from investment advisors to navigate complex markets, create personalized investment strategies, and maximize returns. However, one critical factor to understand before hiring an investment advisor is their fees.

Investment advisor fees can significantly impact your investment returns over time. Knowing how these fees work, what types are charged, and how to evaluate them can help you make informed decisions, avoid surprises, and get the best value for your money.

In this comprehensive guide, we’ll explain:

- What investment advisor fees are

- Common fee structures and how they affect your portfolio

- How to evaluate fee transparency and fairness

- Tips for negotiating and minimizing fees

- Pros and cons of different fee models

- How fees impact your overall investment performance

What Are Investment Advisor Fees?

Investment advisor fees are charges you pay to a professional or firm that manages your investments or provides financial advice. These fees compensate the advisor for their expertise, services, and the time they spend managing your portfolio.

Because these fees come directly out of your investment returns or assets, understanding them is crucial to preserving your wealth.

Why Do Investment Advisors Charge Fees?

Advisors charge fees to cover:

- Portfolio management and rebalancing

- Research and analysis of investment options

- Personalized financial planning and goal setting

- Administrative tasks and compliance

- Access to professional expertise and advice

Fees are a trade-off for potentially better investment returns, risk management, and peace of mind.

Common Types of Investment Advisor Fees

Investment advisor fees come in several common structures. Knowing the differences can help you choose what fits your financial situation best.

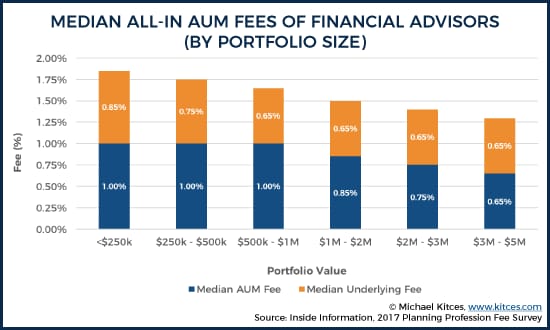

1. Assets Under Management (AUM) Fees

The most common fee structure is the Assets Under Management (AUM) fee, usually charged as a percentage of your portfolio value annually.

- Typical rate: 0.5% to 2% per year

- How it works: If you have $100,000 invested, a 1% AUM fee costs $1,000 annually.

Pros:

- Aligns advisor incentives with your portfolio growth (advisor earns more if your investments grow).

- Easy to understand and calculate.

Cons:

- Can be costly as your portfolio grows.

- Sometimes incentivizes advisors to prioritize asset gathering over personalized advice.

2. Flat or Fixed Fees

Some advisors charge a fixed fee for specific services or ongoing advice, regardless of your portfolio size.

- Typical rate: $1,000 to $5,000 annually or more, depending on services

- Sometimes billed monthly or quarterly.

Pros:

- Transparent and predictable costs.

- Suitable for clients with smaller portfolios.

Cons:

- Less flexible for clients with fluctuating needs.

- Might not cover all services unless explicitly agreed upon.

3. Hourly Fees

In this model, you pay the advisor for the time they spend working for you.

- Typical rate: $150 to $400 per hour

- Best for clients needing limited or one-time advice.

Pros:

- Pay only for what you use.

- Good for specific questions or plans.

Cons:

- Can add up if ongoing advice is needed.

- Less aligned with investment outcomes.

4. Performance-Based Fees

Some advisors charge fees based on the investment performance, typically a percentage of profits above a benchmark.

- Typical rate: 10% to 20% of gains

- Common in hedge funds or private wealth management.

Pros:

- Aligns advisor pay with your success.

- Motivates strong performance.

Cons:

- Can encourage risky investment behavior.

- Complex to calculate and verify.

5. Commission-Based Fees

In this model, advisors earn commissions from selling financial products such as mutual funds, insurance, or annuities.

Pros:

- No upfront fees to clients in some cases.

Cons:

- Potential conflicts of interest.

- May incentivize selling products with high commissions rather than the best fit for you.

How Do Investment Advisor Fees Affect Your Returns?

Even seemingly small fees can dramatically impact your wealth over time due to compounding effects.

Example:

- Initial investment: $100,000

- Annual return: 7% before fees

- Fee scenarios:

- 0.5% fee → After 20 years = ~$270,000

- 1.0% fee → After 20 years = ~$242,000

- 2.0% fee → After 20 years = ~$186,000

The difference between a 0.5% and 2.0% fee over 20 years can cost you nearly $84,000.

Evaluating Fee Transparency and Fairness

When assessing an advisor, transparency about fees is crucial. Ask:

- What exactly do you charge and how often?

- Are there any hidden fees or additional costs?

- Is the fee negotiable?

- What services are included in the fees?

- How are fees deducted or billed?

A trustworthy advisor will provide a clear Form ADV Part 2 or equivalent disclosure document detailing fees and services.

Tips to Minimize Investment Advisor Fees

- Compare multiple advisors: Fees vary widely; shop around.

- Negotiate fees: Many advisors are open to negotiation, especially for larger portfolios.

- Consider robo-advisors: Automated platforms typically charge 0.25% or less.

- Use flat fee or hourly advisors if your needs are limited.

- Consolidate accounts: Some advisors reduce fees if you consolidate your investments.

- Review fees regularly: Ensure fees remain competitive as your portfolio grows.

Pros and Cons of Different Fee Models

| Fee Model | Pros | Cons | Best For |

|---|---|---|---|

| AUM Fee | Aligns advisor with portfolio growth | Can be expensive for large portfolios | Long-term investors |

| Flat Fee | Predictable costs | May not cover all services | Clients with smaller portfolios |

| Hourly Fee | Pay only for needed advice | Can get costly for ongoing needs | One-time or occasional advice |

| Performance-Based Fee | Motivates advisor performance | Encourages risk-taking | High-net-worth clients |

| Commission-Based | No upfront fees in some cases | Potential conflicts of interest | Clients buying specific products |

Questions to Ask Your Investment Advisor About Fees

- How are your fees calculated?

- Are there any additional charges I should know about?

- Can you provide a fee schedule in writing?

- How do fees impact my overall investment returns?

- Are you a fiduciary, legally obligated to act in my best interest?

- What services am I getting for these fees?

Conclusion

Understanding investment advisor fees is vital to making informed financial decisions. Fees reduce your net returns, so it’s essential to choose a fee structure that aligns with your goals, budget, and investment style. Always prioritize transparency, ask questions, and consider whether the value of the advisor’s services justifies the cost.

Remember, the cheapest option isn’t always the best — but neither is the most expensive. A good advisor should offer fair fees, clear communication, and help you grow your wealth effectively.

By educating yourself about investment advisor fees, you can take control of your financial future and make smart, cost-effective choices that benefit you in the long run.